Interest Rate Hikes Cool Home Price Appreciation While Single-Family Rent Growth Remains Strong

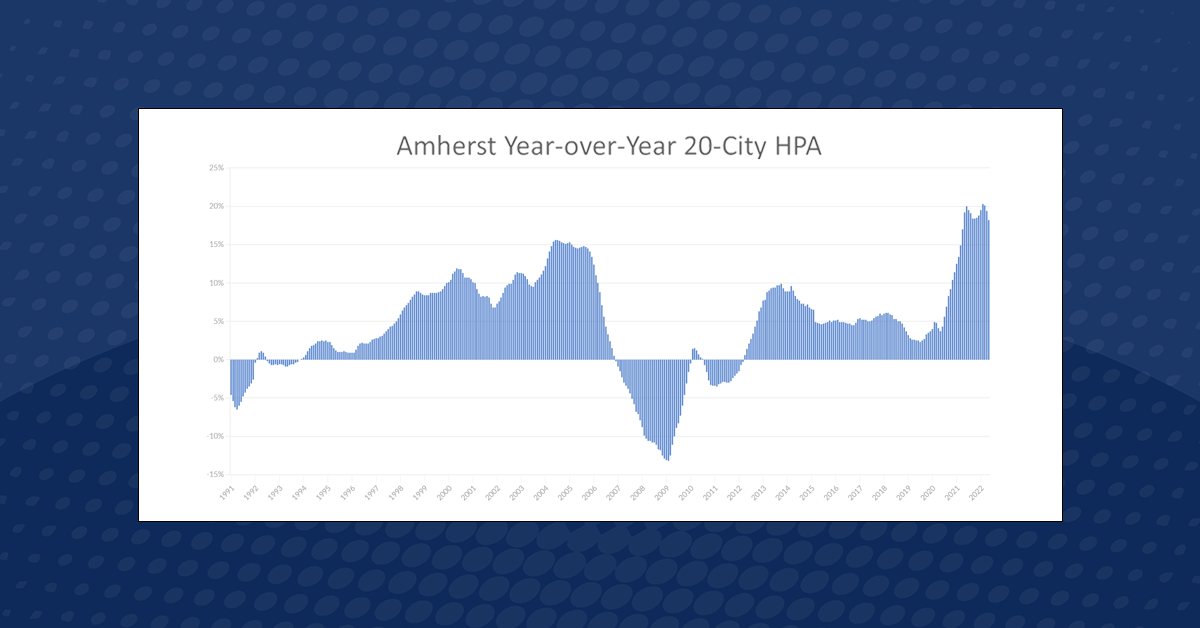

The Federal Reserve’s steep interest rate increase mid-way through June led the average 30-year fixed rate mortgage to rise to 5.7 percent, starting a period of stronger calming.1 Accordingly, the Amherst Home Price Appreciate Index (HPA) cooled down to a year-over-year (YoY) value of 17.1 percent in June 2022, 90 basis points (bp) lower than the month prior.

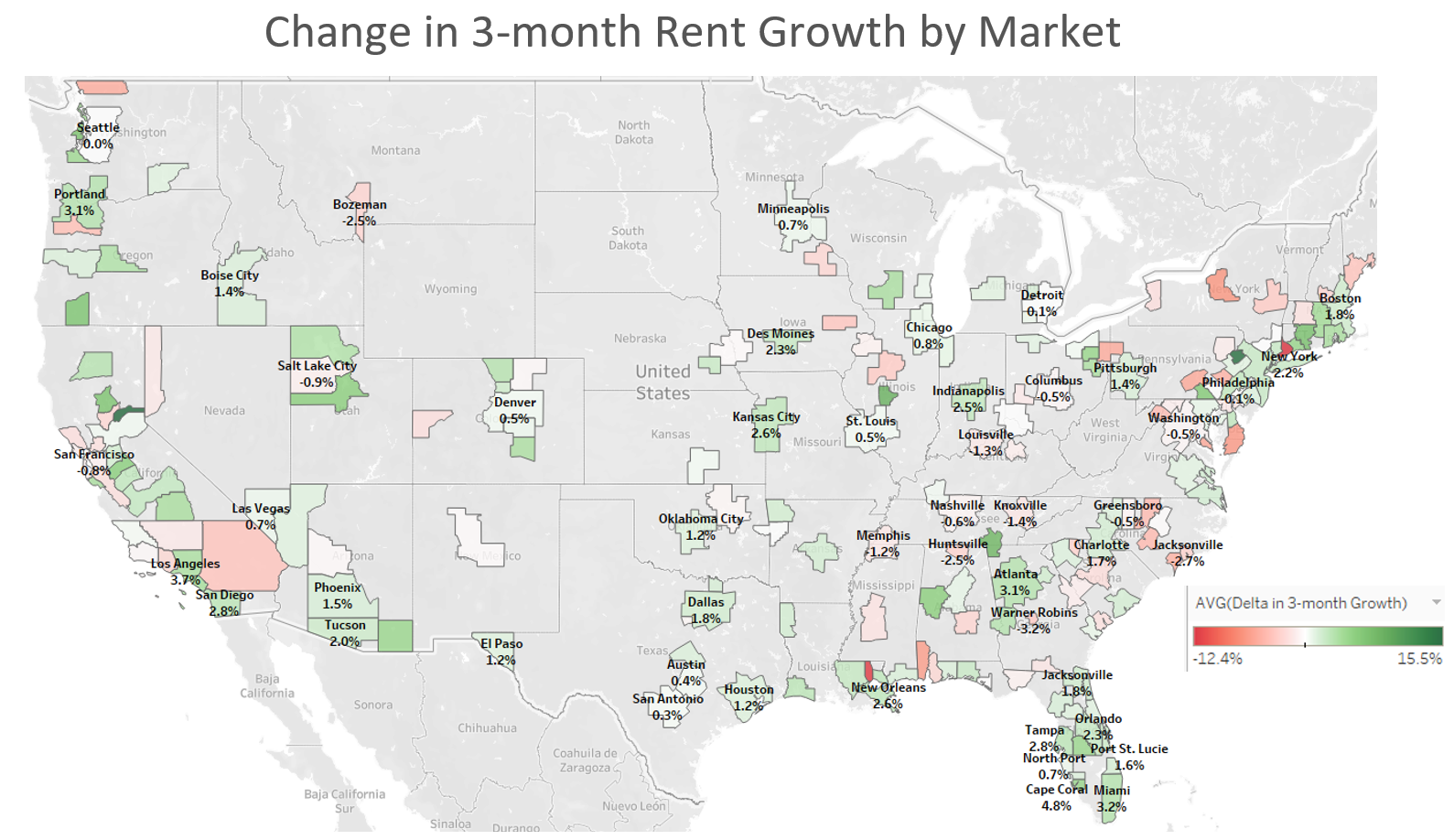

Other metrics are consistent with the housing market’s cooling trends, as reflected by the HPA. Absorption rates are down 3.4 percentage points (pp) from May, while the volume of mortgage originations in June is down 17 percent from May to $116.7B.2 Although the ownership market is cooling, most market performance metrics are still above their 2019 values, which was also a strong year for housing, suggesting it will take at least a few more quarters for the full momentum of the Fed’s actions to ripple through the markets.

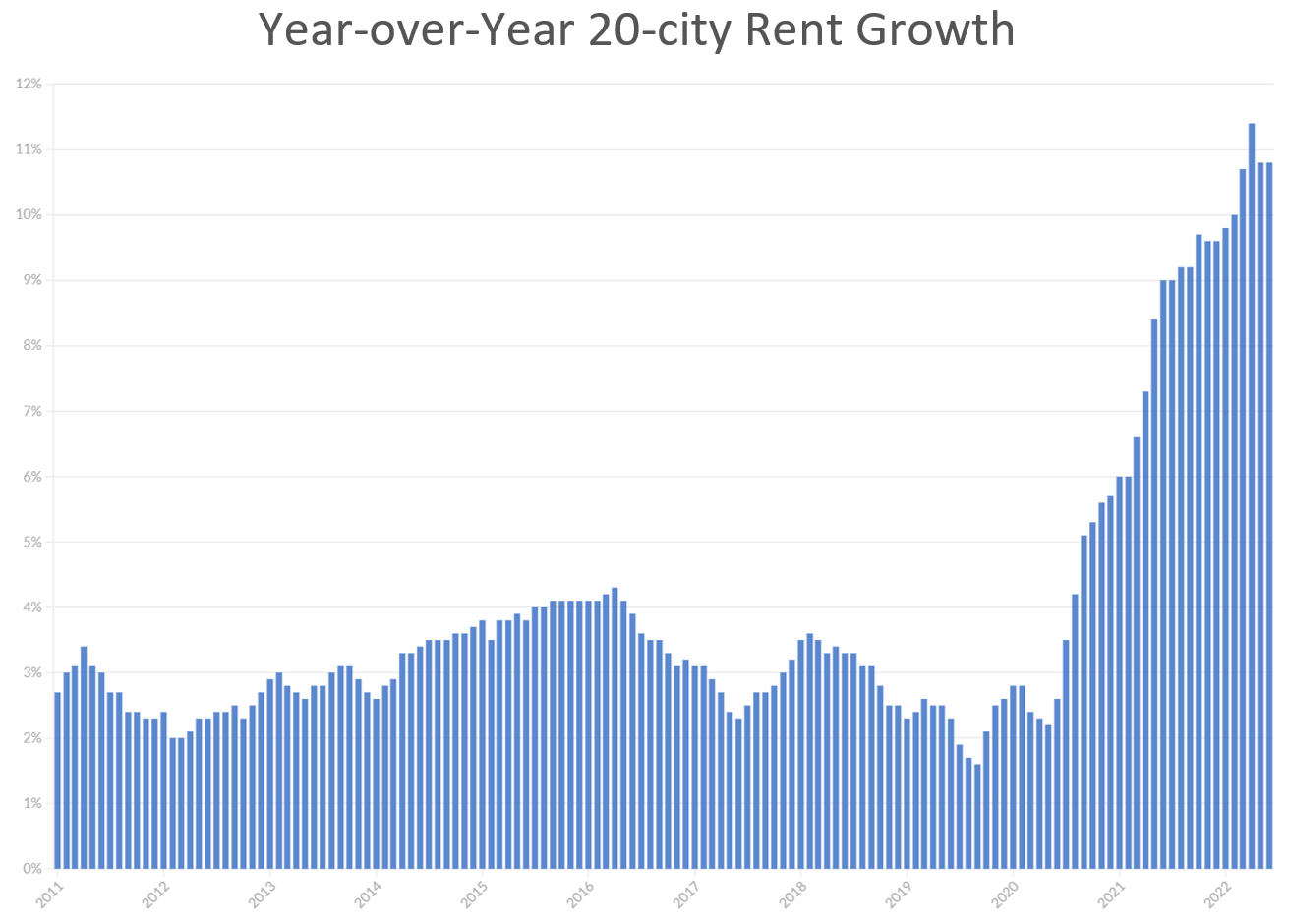

In response to ownership becoming increasingly more expensive and less attainable, Amherst believes rent growth should remain high in the short term as households turn to homes for lease as a more affordable way to access single-family homes. Accordingly, the Amherst Rent Growth Index maintained 10.8 percent YoY growth in June 2022, the same as May growth. However, other indicators show signs of slowing, including 30-day absorption which slid by 1 pp to 48 percent – 12 pp lower than the same time last year.

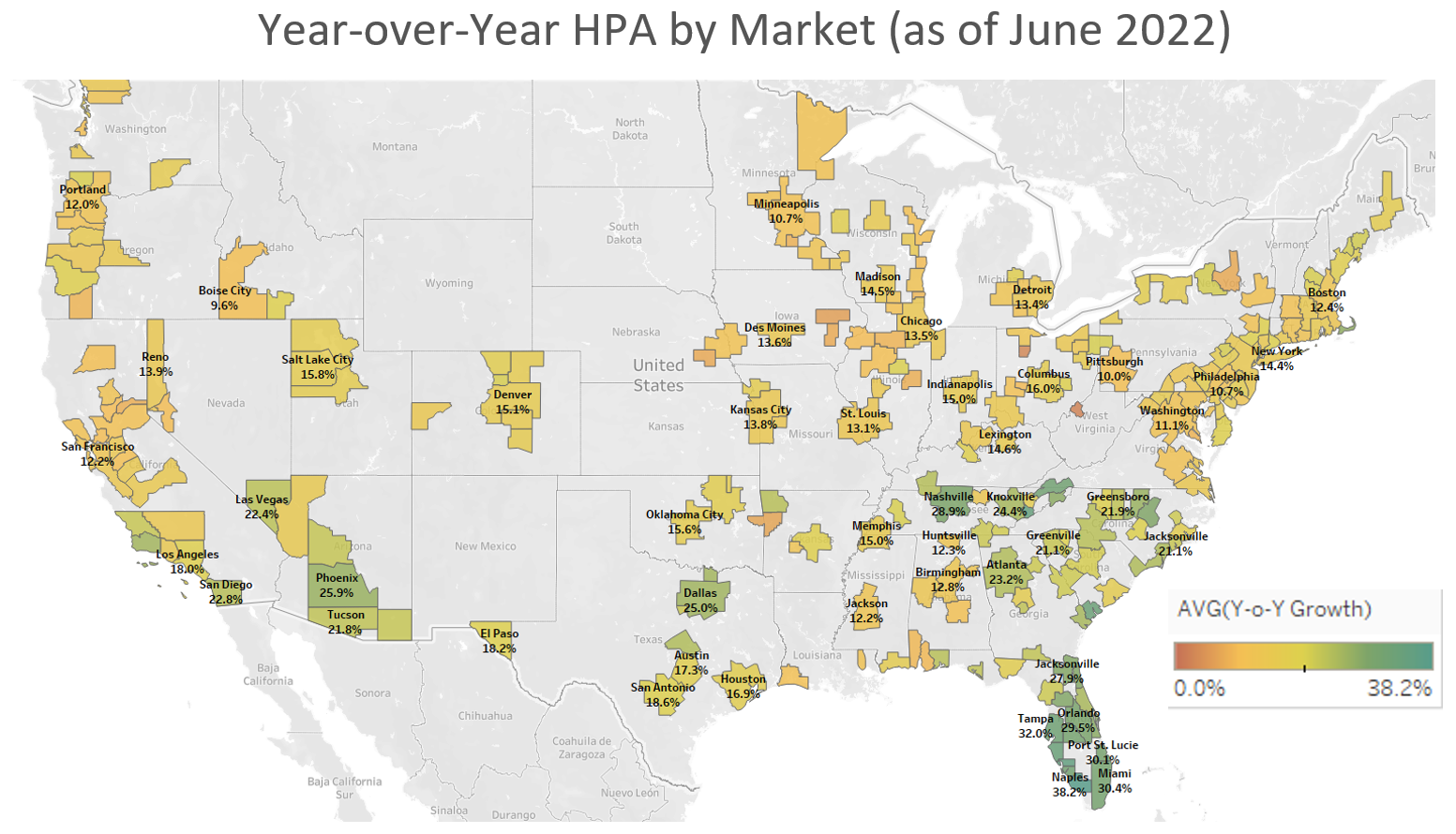

Regional Trends in HPA

The highest growth markets are relatively concentrated, with twelve of the top twenty growth MSAs in Florida and four in Tennessee. Naples, FL and Punta Gorda, FL saw the highest growth in the U.S., at 38.2 percent and 35.3 percent, respectively. Sevierville, TN came in third, with YoY HPA of 34.3%. Johnson City, TN also appeared in the top 20, with YoY HPA growth of 27.1 percent. The remaining states with markets in the top 20 include South Carolina, North Carolina, Massachusetts, and Arizona.

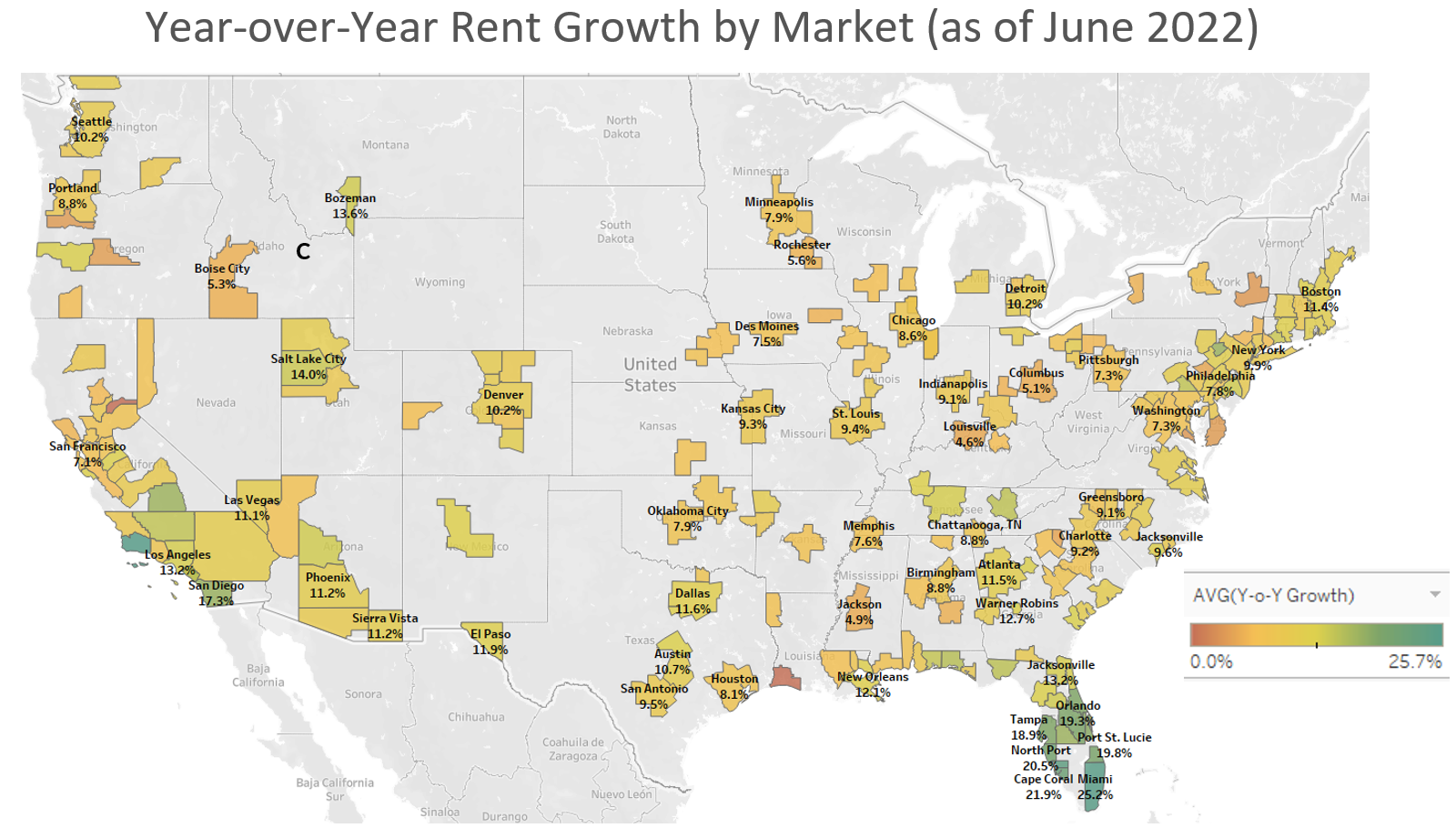

Regional Trends in Rent Growth

June began to see marked divergence in geographical overlap between single-family rent growth and HPA. Outside of the strong markets in Florida, there were no similarities between the top-20 markets for HPA and rent growth. In fact, with YoY rent growth of 25.7 percent, the market with the fastest growing rent was Santa Maria, CA, which does not appear among the top growth HPA MSAs. Although the next nine markets are in Florida, California markets dominate positions eleven through 20. Outside of California and Florida, states with markets in the top 20 include Pennsylvania and Tennessee.

Conclusion

We do not believe a sudden correction will materialize in the forthcoming quarters. The July 2022 employment figures released by the Bureau of Labor Statistics (BLS) suggest that employment has improved. Unemployment inched down by 10 bps to 3.5%, non-farm employment is back to pre-pandemic levels, long-term unemployed decreased, and hourly earnings continued to increase by 5.2% YoY. Despite efforts by the Fed to tame inflation, July’s employment outcomes suggest the economy carries a fundamental, strong momentum. In response, we anticipate that the Fed will raise interest rates, which will slow HPA even further.

1Federal Reserve Bank, Implementation Note Issued June 15, 2022

Freddie Mac, 30-Year Fixed Rate Mortgage Average in the United States, sourced from St Louis Federal Reserve Bank

2MLS data tabulated by Amherst Research, June 2022. EMBS data tabulated by Amherst Research, June 2022

Data Details

The Amherst Home Price Appreciation Index (HPA) tracks home price changes in the same 20 Metropolitan Statistical Areas (MSAs) that are used to construct the S&P CoreLogic Case-Shiller 20-City Index. Amherst also tracks market-level home-price changes to produce home price indexes for over 200 Core-Based Statistical Areas (CBSA) in the United States. The index is published on a monthly basis and is based on the Case Shiller repeat-sales methodology. Unlike the indices published by S&P CoreLogic Case-Shiller and the Federal Housing Finance Agency (FHFA), the Amherst HPA is a distressed-free index which does not include price changes due to foreclosures, short-sales, bank repossession, and REO resale. The use of Multiple Listing Services (MLS) data that are supplemented by CoreLogic off-market data allow the HPA to have a timelier look at monthly shifts in the housing market than some other leading market indices.3

The Amherst Rent Growth Index follows single-family detached homes rent price changes for the same MSAs that are used to construct the S&P CoreLogic Case-Shiller 20-City Index. Amherst also follows market-level statistics for over 150 CBSAs in the United States. The index is published every month and uses a repeat-rent methodology similar to the one employed for the Amherst HPA. The index incorporates both MLS and Altos rental data to produce a timely rent index.

Due to the early nature of our estimates, our indexes for prior months can change.

3At the time of writing this June 2022 housing market report, the S&P Case Shiller Index has been released up through May 2022.

Important Disclosures

The comments provided herein are a general market overview and do not constitute investment advice, are not predictive of any future market performance, are not provided as a sales or advertising communication, and do not represent an offer to sell or a solicitation of an offer to buy any security.

Similarly, this information is not intended to provide specific advice, recommendations or projected returns of any particular product of The Amherst Group LLC (“Amherst”) or its subsidiaries and affiliates.

These views are current as of the date of this communication and are subject to rapid change as economic and market conditions dictate. Though these views may be informed by information from sources that we believe to be accurate and reliable, we can make no representation as to the accuracy of such sources nor the completeness of such information. Past performance is no indication of future performance. Investments in mortgage related assets are speculative and involve special risks, and there can be no assurance that investment objectives will be realized or that suitable investments may be identified. Many factors affect performance including changes in market conditions and interest rates and in response to other economic, political, or financial developments. An investor could lose all or a substantial portion of his or her investment. No investment process is free of risk and there is no guarantee that the investment process described herein will be profitable. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

Author: Gene Burinskiy | Vice President, Research & Data Journalism | The Amherst Group

Contributor: Thu Vo | Staff Financial Data Scientist | The Amherst Group