Strong Metro Demand for Suburban Homes Drives High Home Price and Rent Growth

Demand for suburban homes from consumers living in urban areas supported strong February home price and rent growth. Suburbs of larger urban cores were the highest appreciating home markets in February 2022, which follows pandemic-induced migration flows. Between the onset of the COVID-19 pandemic in Q1 2020 and Q2 2021, more than 2.4 million people chose to relocate from high-cost large metropolitan areas to more spacious and affordable single-family homes in lower-cost metros.1,2 Before the pandemic, urban outflow primarily consisted of lower-income households who were being priced out of high-cost cities. This has shifted, with more high-income households departing for the suburbs than low-income households. Although the cohort of moving and buying consumers broadened throughout 2021, wealthier households, including early retirees, continued moving to the sunbelt and other retirement destinations.3 These migration trends are underscored by Fannie Mae’s findings on suburban housing inventories, which shrank 30% faster than urban counterparts during the pandemic.4 Unsurprisingly, home prices and rents are growing in those cities that saw an influx of new residents.

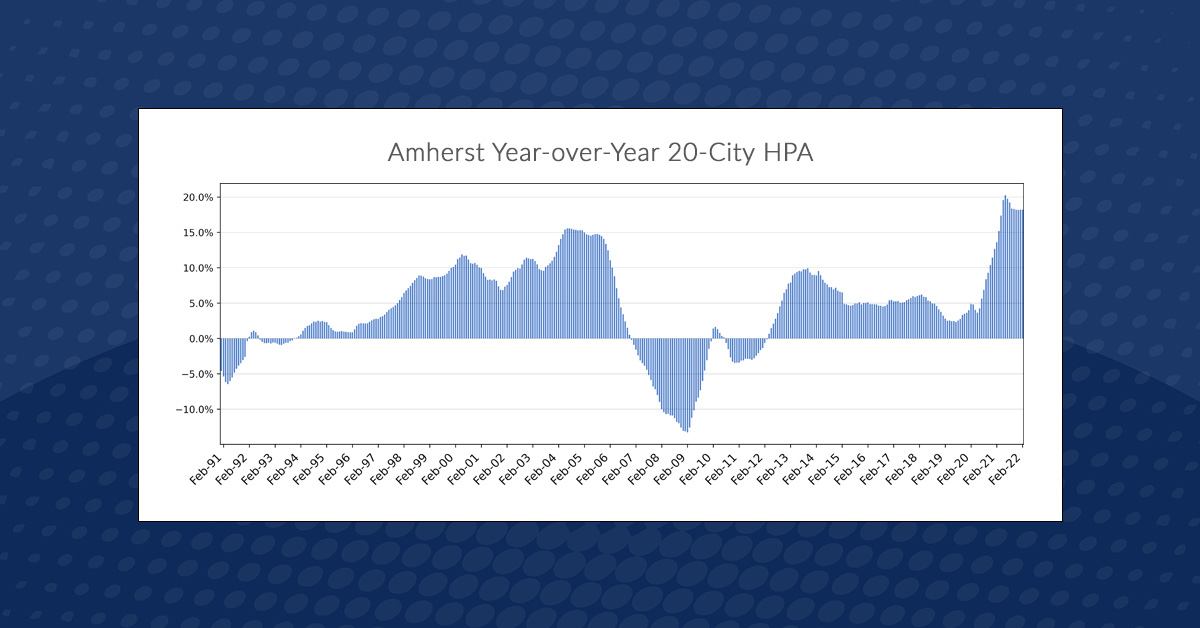

Amherst Home Price Appreciation Index

At the national scale, the 20-city Amherst Home Price Appreciation Index (HPA) grew 18.2% year-over-year (YoY) in February 2022 as a result of persistently high consumer demand and low inventories. This is in line with the 18% growth prevalent since September 2021 and is only a slight decline since the summer of 2021. However, this high growth is not uniform across the U.S.

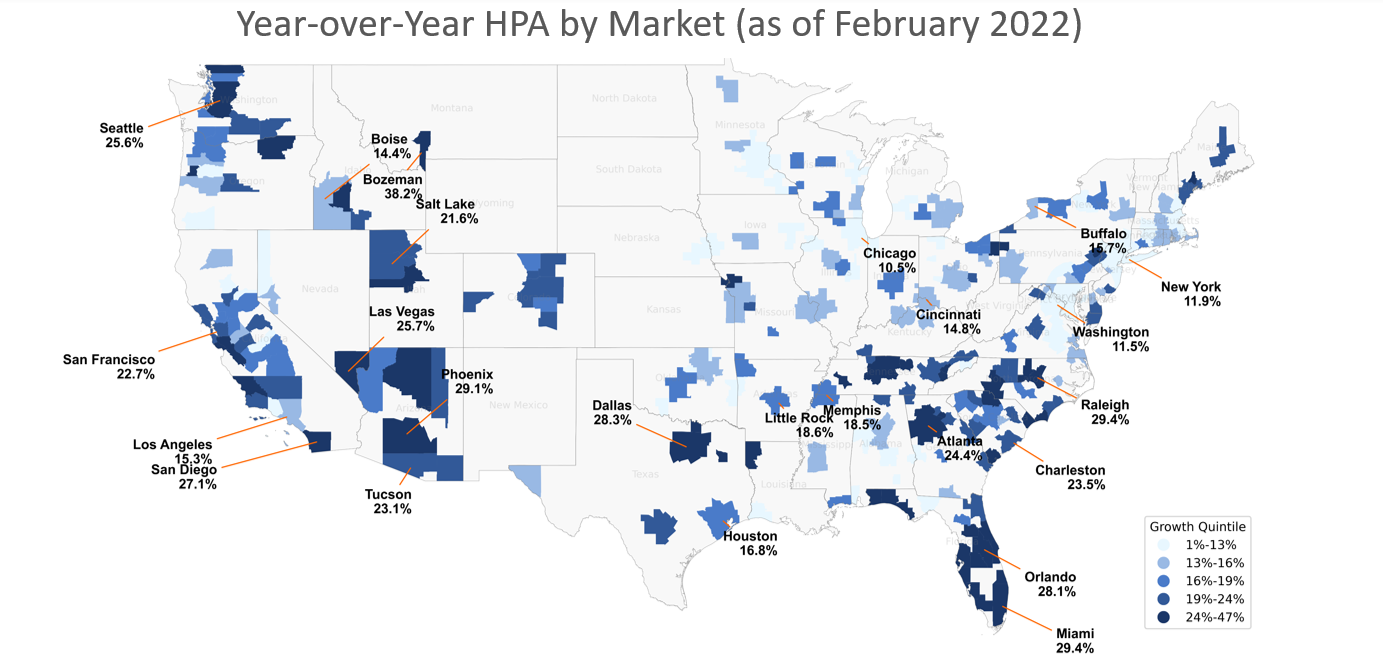

Data suggest that suburbs near larger metros experienced higher HPA growth in February 2022 than the nearby urban centers. Morristown TN, a suburb of Knoxville, experienced YoY growth of 41.2% in the U.S., while Bozeman, MT returned to the top five at 38.2% YoY growth. More saliently, Bozeman’s suburban neighbor Mountain Home, MT made it to the top 10 at 31.5%. The remainder of the top five markets with the highest February home price growth were all Fort Myers, FL suburbs. Naples, FL grew at 47% YoY, Punta Gorda, FL grew 38.3%, and North Port, FL grew 37.3% in February 2022.

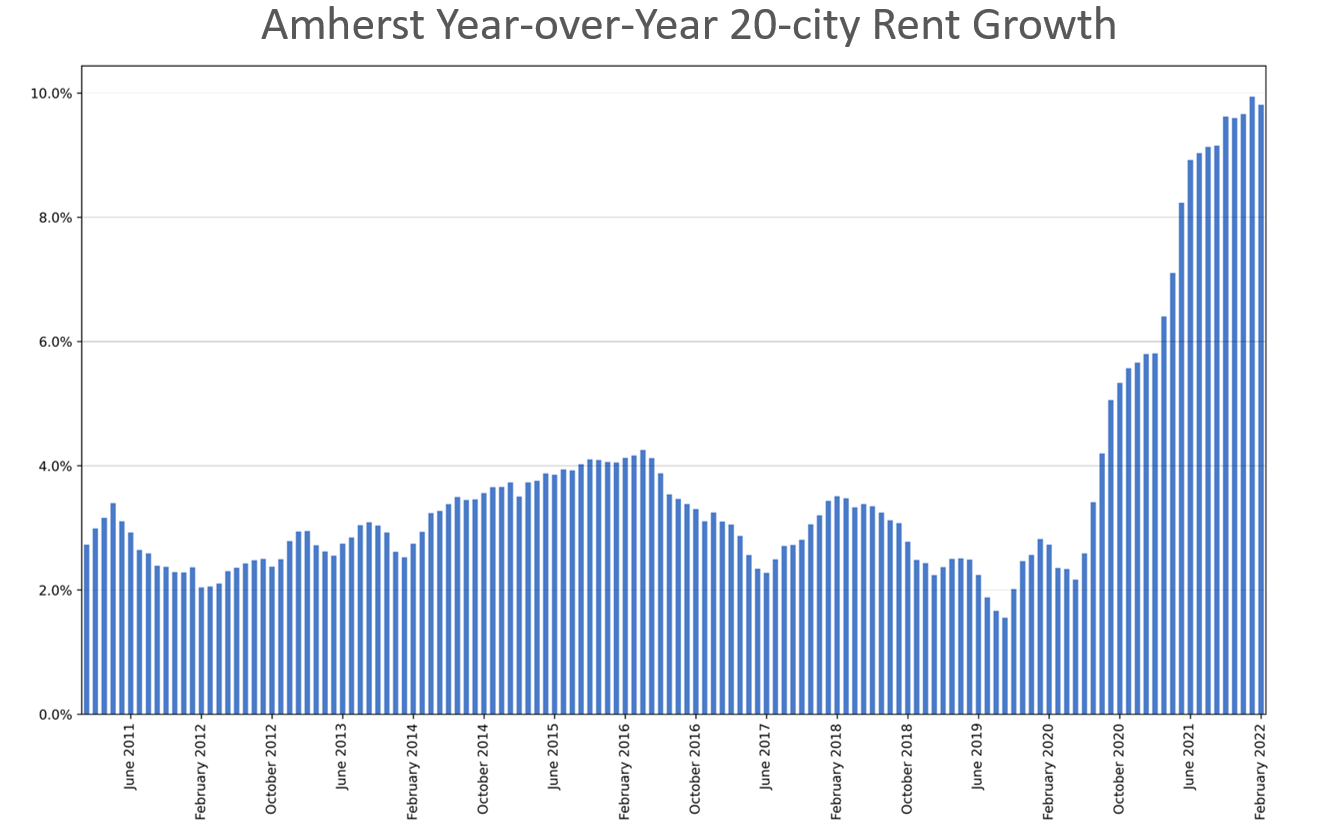

Amherst Rent Growth Index

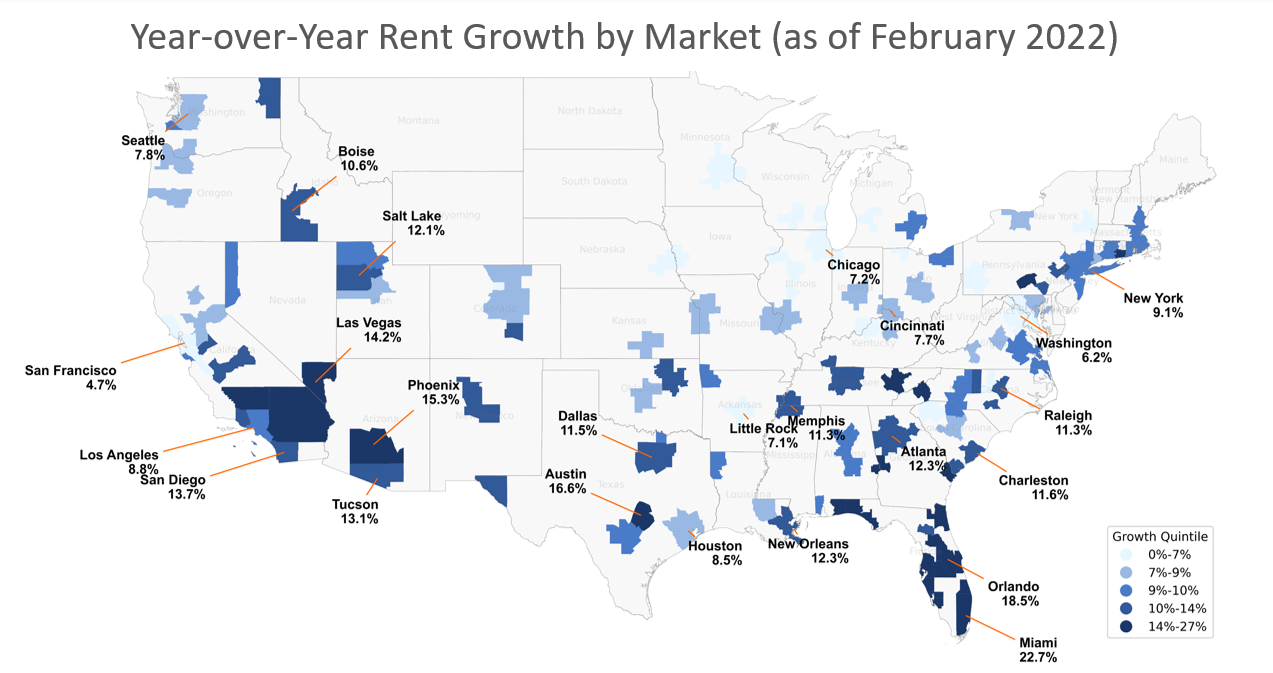

February 2022 rents grew by 9.8% YoY, according to the 20-city Amherst Single-Family Rent Growth index. This is a slight decrease from the prior month’s 9.9% YoY increase, but in line with growth trends since summer 2021 of over 9%.

Single-family rent growth was still the highest in Florida. The Florida suburbs of Crestview, Cape Coral, Port St. Lucie, and North Port experienced rent growth ranging from 20.9% to 27.4%. Additionally, Miami experienced rent growth of 22.7%. This is not surprising, as analyses of migration in the U.S. consistently show Florida as one of the most popular destinations since the pandemic’s start. In the first four quarters of the pandemic, Fort Myers, Florida alone saw a net increase of 10,240 households, the equivalent of almost 2% of its workforce.5 As a result, Bakersfield, CA is the only market with rent growth in the top 12 that is not in Florida.

1Stephan Whitaker. Migrants from High-Cost, Large Metro Areas during the COVID-19 Pandemic, Their Destinations, and How Many Could Follow. Cleveland Federal Reserve Bank. March 25, 2021. [link].

2Stephan Whitaker. Date Updated to U.S. Migration Patterns During the Pandemic. Cleveland Federal Reserve. August 26, 2021. [link].

3Emergence of a ‘New Norma’ Housing Market Begins. Economic & Housing Outlook. Fannie Mae. January 19, 2022 [link]

4“Has An Urban Exodus Occurred? Residential Environment Trends Shaping the Future of Where We Live.” Freddie Mac, Research note, July 12, 2021. [link]

5Stephan Whitaker. Data Updates to U.S. Migration Patterns During the Pandemic. Federal Reserve Bank of Cleveland. August 26, 2021. [link]

Data Details

The Amherst Home Price Appreciation Index (HPA) tracks home price changes in the same 20 Metropolitan Statistical Areas (MSAs) that are used to construct the S&P CoreLogic Case-Shiller 20-City Index. Amherst also tracks market-level home-price changes to produce home price indices for over 200 Core-Based Statistical Areas (CBSA) in the United States. The index is published on a monthly basis and is based on the Case Shiller repeat-sales methodology. Unlike the indices published by S&P CoreLogic Case-Shiller and the Federal Housing Finance Agency (FHFA), the Amherst HPA is a distressed-free index which does not include price changes due to foreclosures, short-sales, bank repossession, and REO resale. The use of Multiple Listing Services (MLS) data that are supplemented by CoreLogic off-market data allow the HPA to have a timelier look at monthly shifts in the housing market than some other leading market indices.6

The Amherst Rent Growth Index follows single-family detached homes rent price changes for the same MSAs that are used to construct the S&P CoreLogic Case-Shiller 20-City Index. Amherst also follows market-level statistics for over 150 CBSAs in the United States. The index is published every month and uses a repeat-rent methodology similar to the one employed for the Amherst HPA. The index incorporates both MLS and Altos rental data to produce a timely rent index.

Due to the early nature of our estimates, our indices for prior months can change.

6At the time of writing this February 2022 housing market report, the S&P Case Shiller Index has been released up through January 2022.

Important Disclosures

The comments provided herein are a general market overview and do not constitute investment advice, are not predictive of any future market performance, are not provided as a sales or advertising communication, and do not represent an offer to sell or a solicitation of an offer to buy any security.

Similarly, this information is not intended to provide specific advice, recommendations or projected returns of any particular product of The Amherst Group LLC (“Amherst”) or its subsidiaries and affiliates.

These views are current as of the date of this communication and are subject to rapid change as economic and market conditions dictate. Though these views may be informed by information from sources that we believe to be accurate and reliable, we can make no representation as to the accuracy of such sources nor the completeness of such information. Past performance is no indication of future performance. Investments in mortgage related assets are speculative and involve special risks, and there can be no assurance that investment objectives will be realized or that suitable investments may be identified. Many factors affect performance including changes in market conditions and interest rates and in response to other economic, political, or financial developments. An investor could lose all or a substantial portion of his or her investment. No investment process is free of risk and there is no guarantee that the investment process described herein will be profitable. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

Author: Gene Burinskiy | Vice President, Research & Data Journalism | The Amherst Group

Contributor: Thu Vo | Staff Financial Data Scientist | The Amherst Group