Tight Housing Supply and High Demand Sustain Strong Home Price and Rent Growth

The high consumer demand for homes amid supply shortages of yesteryear continues to ring loud this new year. Homes in 2021 were whisked off the market by consumers at a pace not seen since the early 2000s. The 90-day home sales velocity jumped by 39% from its 2019 levels to 76% in 2021.1 As a result, the December 2021 for-sale inventory ended 33% lower than it did in 2019 despite ramped up production of new homes.2,3 This high demand is primarily driven by individuals who intend to make their purchased houses their home. For every 100 homes sold in 2021, 71 were sold to individuals and 28 were sold to small investors. Only 1 out of 100 homes was sold to an institutional investor.4,5

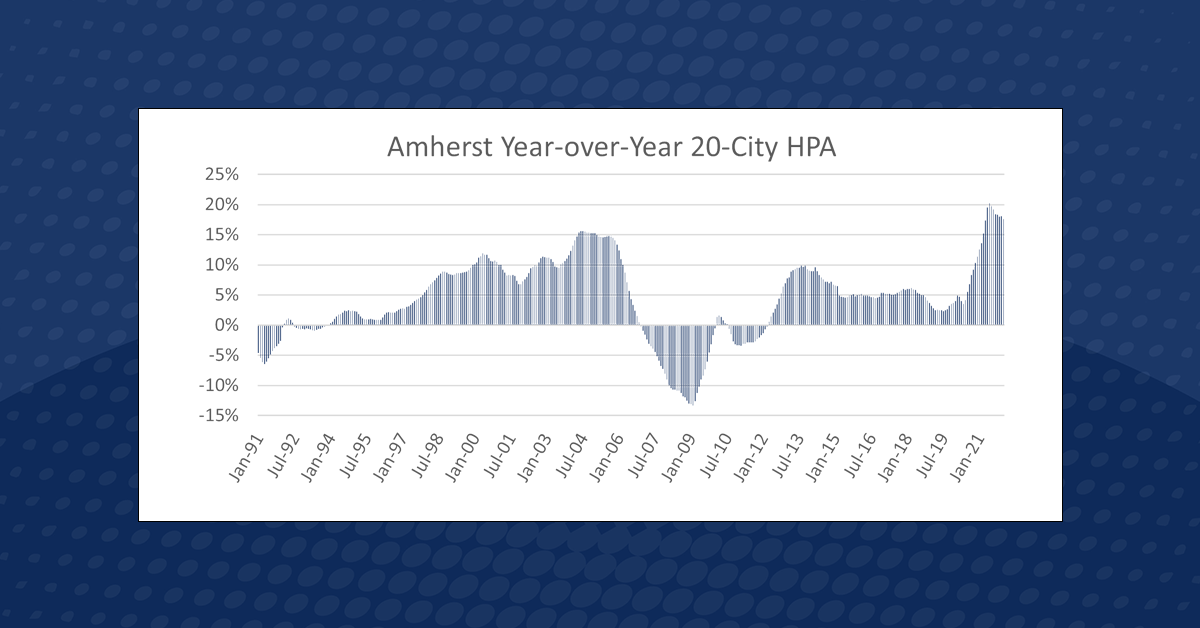

Construction companies are ramping up production to address the supply shortage but face labor and material shortages. Amherst Research estimates the construction market is short 1.5 million workers needed to keep pace with the new levels of construction activity.6 Shortages of everything from doors and windows to refrigerators have delayed construction, while simultaneously increasing input prices that raise construction costs.7 Lumber prices alone more than doubled from their pre-pandemic levels.8 The confluence of high demand and hampered supply sustained Year-on-Year (YoY) home price appreciation of 17.6% in January, according to the 20-City Amherst Home Price Appreciation Index (HPA).

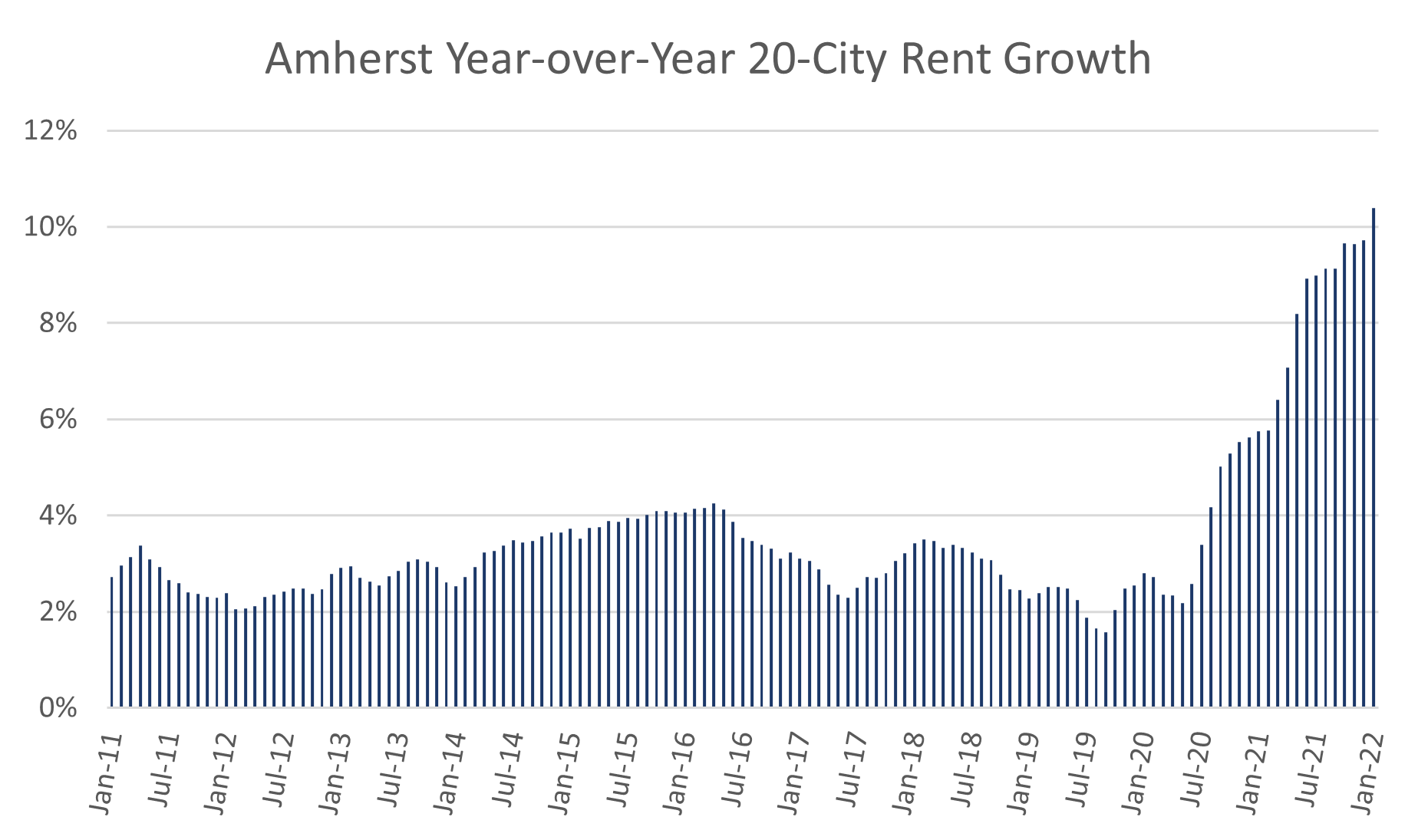

The single-family rental market has followed a similar trajectory. According to Amherst Research, the for-lease inventory in December 2021 was down 37% from its pre-pandemic December 2019 levels due to high absorption rates. At 77%, the average 60-day velocity in 2021 was 28% higher than in 2019.9 This unwavering demand caused YoY rent growth to hit a new high of 10.4% in January, according to the Amherst Rent Growth Index. More notably, the leap of 7 percentage points from November’s YoY growth marks a departure from the more languid autumn rent growth acceleration. Such growth spurts tend to occur every few months followed by slower growth acceleration. Whether this foreshadows a new phase in high rent growth remains to be seen.

Amherst Home Price Appreciation Index

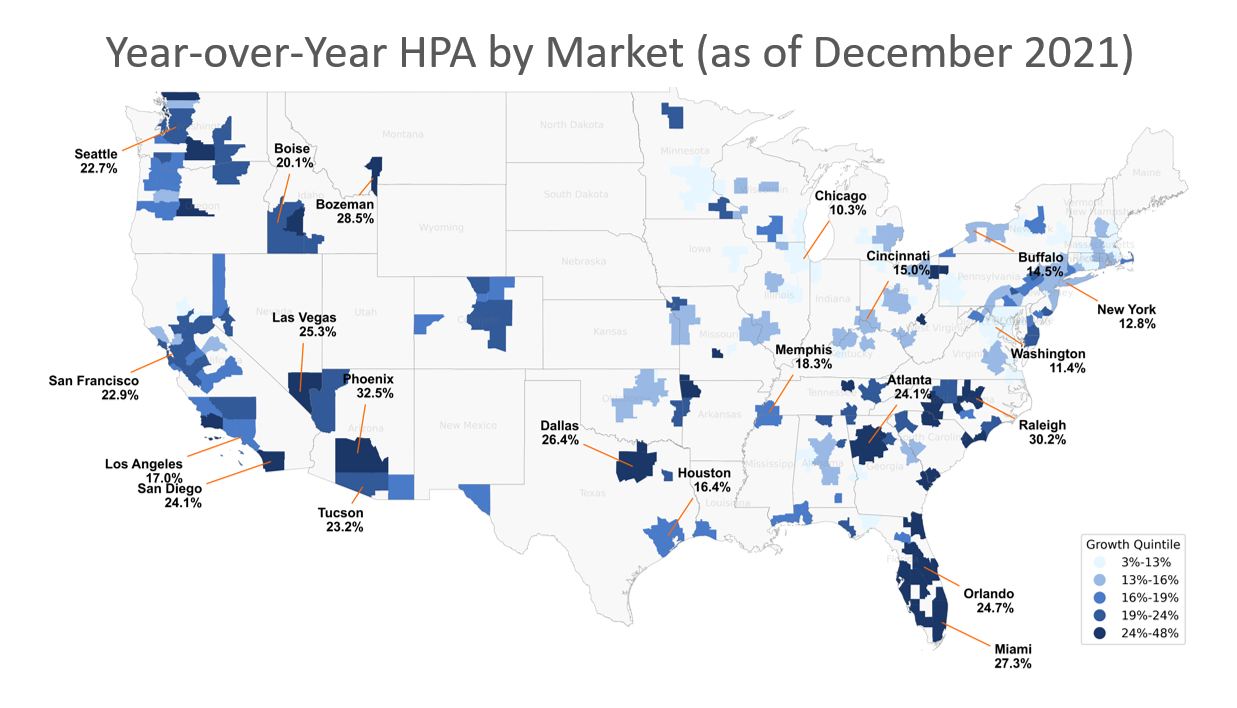

Amherst’s HPA index showed most markets tracking above 10%, with Florida entering the new year as the state with the fastest appreciating markets. Naples, FL had the nation’s highest January HPA at 47.7%, followed by Punta Gorda, FL at 40.1% and Cape Coral, FL at 33.6%. The Southeast and suburban West Coast regions remain the most rapidly expanding markets.

Amherst Rent Growth Index

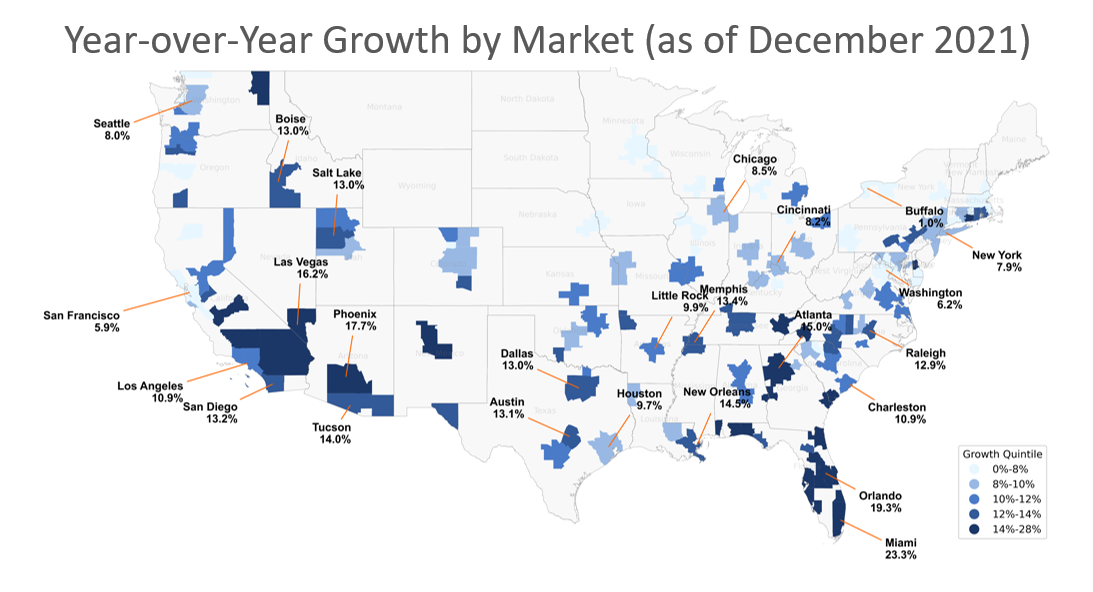

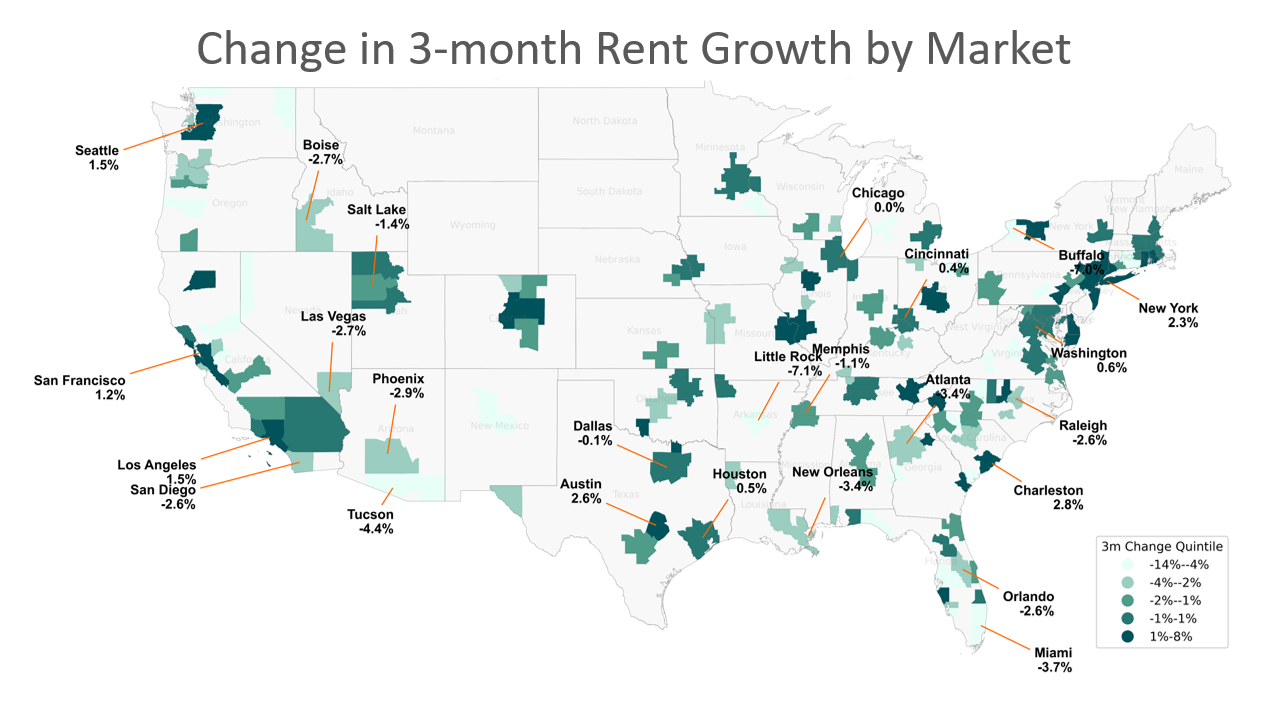

The fastest single-family rent growth in January was also in Florida, with its five fastest growing markets at YoY rent growth ranging from 28.9% in North Port to 21.3% in Tampa. Of the nearly 150-tracked U.S. markets, most experienced YoY rent growth over 5%, with the Southeast and western suburban markets growing markedly faster than the rest of the U.S. Since supply shortages and high absorption continue to prevail, Amherst Research does not anticipate slowed rent growth in early 2022. Moreover, if interest rates rise in response to high inflation, Amherst believes demand for single-family rentals may grow even more.

1Amherst estimates as of January 2022 based on publicly available information, includes listings up to September 2021.

2Amherst tabulation of Corelogic MLS data as of December 2021.

3Amherst Tabulation of Metro Study data as of Q3 2021.

4Small investors are defined as owners who are not institutional investors and whose addresses do not coincide with the purchased property.

5Amherst Tabulation of CoreLogic Transactions Data as of December 31, 2021.

6U.S. Bureau of Labor Statistics as of December 2021.

7National Association of Home Builders Report on results from the May 2021NAHB/Walls Fargo Housing Market Index Survey.

8National Association of Home Builders Report based on Producer Price Index (PPI) figures from the Bureau of Labor Statistics as of February 15, 2022.

9Amherst estimates as of January 2022 based on publicly available information. Last data point in September 2021.

Data Details

The Amherst Home Appreciation Price Index (HPA) tracks home price changes in the 20 Metropolitan Statistical Areas (MSAs) that are used to construct the S&P Case Shiller 20-city Index as well as over 200 Core-Based Statistical Areas (CBSA) in the United States. The HPA is published on a monthly basis and is based on the Case Shiller repeat-sales methodology. Unlike the HPA published by S&P Case Shiller Weiss, Corelogic, and the Federal Housing Finance Agency (FHFA), Amherst HPA is a distressed-free index which does not include price changes due to foreclosures, short-sales, bank repossession and REO resale. The use of Multiple Listing Services (MLS) data that are supplemented by Corelogic off-market data allow the HPA to have a timelier look at monthly shifts in the housing market than some other leading market indices.10

The Amherst Rent Growth Index is generated and maintained by Amherst and tracks rent price changes of Single Family Detached (SFD) homes in the 20 Metropolitan Statistical Areas (MSAs) that are used to construct the S&P Case Shiller Index as well as over 150 CBSAs in the United States. The Amherst Rent Growth Index is published every month and uses a repeat-rent methodology similar to the one employed for the Amherst HPA. The index incorporates both MLS and Altos rental data to produce a timely rent index. The rent index relies on tracking rent price changes of the same house over time. For each lease, a search is conducted to find rent price from the previous lease of the same house. If an earlier lease is found, the two leases are paired into a “lease pair.” Lease pairs are designed to track rent price changes over time for the same house, while holding the quality and size of each house constant. After pairs are formed, the index is calculated under a weighted least square framework, in which weights are based on rent price anomalies and time interval within pairs. The index is based on re-leases on the same properties that are put on the market and therefore does not include any repeat leases which are renewals.

Due to the early nature of our estimates, our indexes for prior months can change.

10At the time of writing this January 2022 housing market report, the S&P Case Shiller Index has been released up through December 2021.

Important Disclosures

The comments provided herein are a general market overview and do not constitute investment advice, are not predictive of any future market performance, are not provided as a sales or advertising communication, and do not represent an offer to sell or a solicitation of an offer to buy any security.

Similarly, this information is not intended to provide specific advice, recommendations or projected returns of any particular product of The Amherst Group LLC (“Amherst”) or its subsidiaries and affiliates.

These views are current as of the date of this communication and are subject to rapid change as economic and market conditions dictate. Though these views may be informed by information from sources that we believe to be accurate and reliable, we can make no representation as to the accuracy of such sources nor the completeness of such information. Past performance is no indication of future performance. Investments in mortgage related assets are speculative and involve special risks, and there can be no assurance that investment objectives will be realized or that suitable investments may be identified. Many factors affect performance including changes in market conditions and interest rates and in response to other economic, political, or financial developments. An investor could lose all or a substantial portion of his or her investment. No investment process is free of risk and there is no guarantee that the investment process described herein will be profitable. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

Author: Gene Burinskiy | Vice President, Research & Data Journalism | The Amherst Group

Contributor: Thu Vo | Staff Financial Data Scientist | The Amherst Group